Dual Mandate Says No Major Changes Coming

In 1977, Congress amended The Federal Reserve Act, stating the monetary policy objectives of the Federal Reserve are “to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates”.

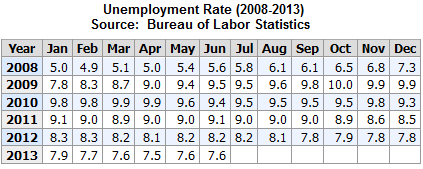

Maximum Employment – Not There Yet

How close is the Fed to meeting the objective of maximum employment? Not all that close. Ben Bernanke reiterated last week that, “There will not be an automatic increase in interest rates when unemployment hits 6.5 percent.” Where is the unemployment rate now? On July 5, it was reported as 7.6%, or well above the minimum threshold of improvement noted by the Fed.

Technicals Improve On Bernanke Remarks

Stocks (SPY) were on the ropes technically after the close on Monday, June 24. Since then, things have improved significantly. The most powerful bullish catalyst came from Ben Bernanke last week:

“Highly accommodative monetary policy for the foreseeable future is what’s needed for the U.S. economy.”

This week’s video describes the bullish migration that has taken place over the last three weeks (see 7:53 mark for specific technical changes):

Inflation Remains In Check

The 1977 amendment to The Federal Reserve Act instructs the Fed to balance “stable prices” with “maximum employment”. Stable prices speak to the inflation rate. Is inflation an imminent threat to the Fed’s easy money policies? No.

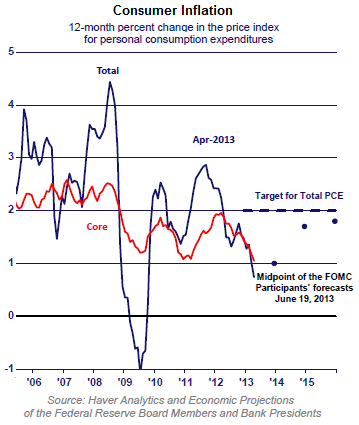

Deflation Not Off Fed’s Radar

Deflationary spirals are very difficult to contain and reverse – just ask the Japanese. Therefore, the Fed does not want a zero inflation environment. The Fed would prefer to see inflation in the neighborhood of 2%. As shown in the chart from the Federal Reserve Bank of Chicago below, inflation is expected to remain below 2% for some time, which means the Fed can continue to pursue their employment mandate with an easy money stance.

Does The Market Fear Inflation?

The chart below shows the performance of gold (GLD) relative to Treasury bonds (TLT). Since gold is often used as a hedge against inflating paper currencies, it is logical to assume GLD would be in greater demand relative to conservative Treasury bonds if fears of future inflation were significant.

Tapering Is About Bubble Management

Our guess is the tapering dialogue at the Fed is more about escalating fears of another round of asset bubbles rather than confidence in the economy or fears about escalating inflation. Therefore, the Fed may still announce some tapering at their September meeting. However, any tapering statement will most likely be accompanied by a pledge to support the economy with low rates for an extended period.

Investment Implications

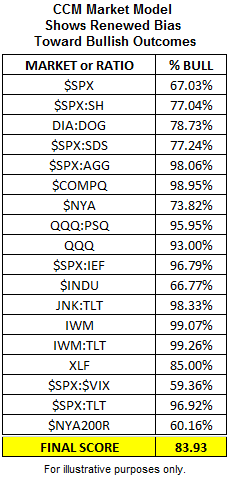

Our market model has moved from a heavy bearish bias on June 24 back to a bullish stance. One component of the model tracks the technical health of the ETFs and markets listed in the table below. A reading of 83.93 (scale 0 to 100) tells us to continue to err on the bullish end of the spectrum.

As long as the markets continue to favor a risk-on allocation, we will continue to overweight U.S. stocks and leading sectors, such as financials (XLF), technology (QQQ), and small caps (IJR).

See Also:

- Employment Trends in the US

- Outside the Box: A Stock Market Message from Darth Vader

- Bank Safety: How to Protect Your Cash in Times of Crisis

- Current Inflation Rate

- Current Unemployment Rate