After years of improvements in drilling techniques and impressive “efficiency gains,” there is now evidence that the U.S. shale industry is reaching the end of the road on Well productivity.

A report earlier this month from Raymond James & Associates finds that the U.S. shale industry may be struggling to achieve further productivity gains. If these improvements begin to fizzle out, it could result in “an inflection point in future global oil supply/demand balances,” the investment bank said.

Oil well productivity is “tracking WAY below our model,” analysts Marshall Adkins and John Freeman wrote in the report. They note that U.S. oil production is up less than 100,000 BPD over the first seven months of 2019, compared to the 600,000-BPD increase over the same period in 2018.

The analysts note that over the past eight years, Raymond James has been one of the most aggressive forecasters for U.S. shale growth, and even then, actual output tended to exceed their forecasts. But this year U.S. shale growth is significantly below their prediction.

The reason is that productivity improvements have suddenly come to an end. Since 2010, initial production rates for the first 30 days of production (IP-30) improved by 30 percent annually on average, according to Raymond James. That was largely the result of the “bigger hammer” approach, the bank said. In other words, drillers threw more of everything at the problem – more money, longer laterals, more sand, and more frac stages. Earlier this decade, IP-30 rates were growing by roughly 40 percent per year. But that slowed to 11 percent in 2017 and 15 percent last year.

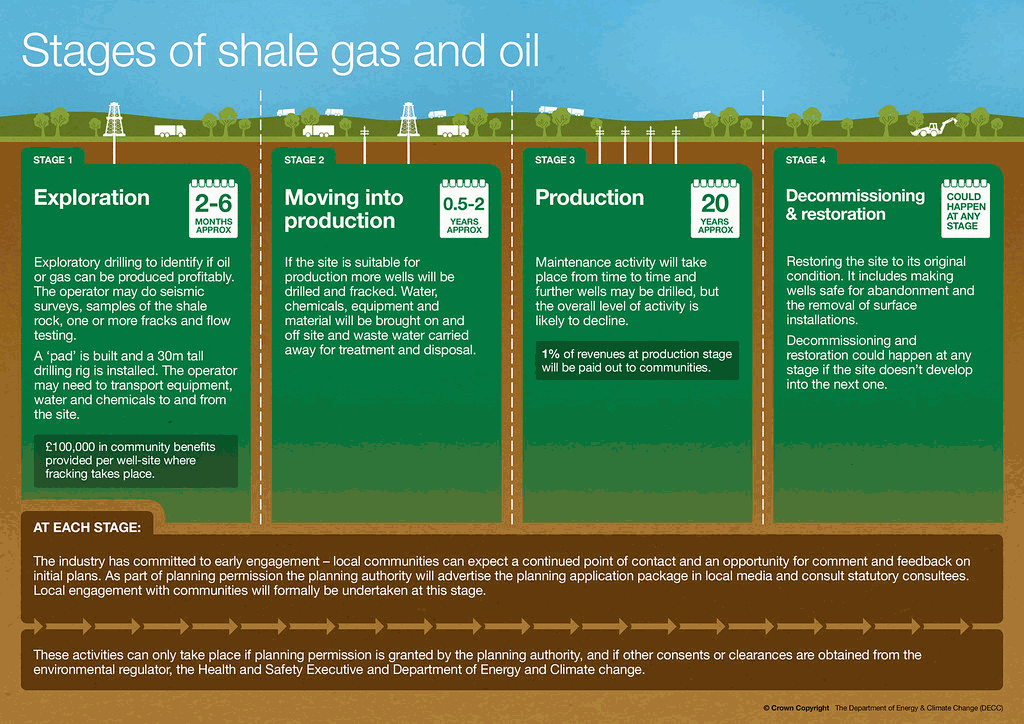

Click for larger Image

However, in the first seven months of 2019, IP-30 rates are up only 2 percent, compared to the 10 percent prediction from Raymond James. Part of the reason is that there is simply a limit to “more, longer and bigger,” the analysts said. “We believe that this represents clear evidence that U.S. well productivity gains are beginning to reach maximum limits and may even roll over in the coming years as the industry struggles to offset well interference issues and rock quality deterioration.” Even 2018 figures may have been a “one-off” increase as the oil majors – Chevron and ExxonMobil – escalated activity.

But perhaps the first 30 days is too short of a timeframe to analyze well productivity. So, the investment bank looked at 90 days of production (IP-90). On that metric, the industry is faring even worse, showing an outright decline of 2 percent in the first half of the year compared to the first six months of 2018.

“Recent Permian IP-90 well productivity trends are especially dire,” the analysts wrote. “While U.S. IP-90s declined 2%, Permian IP-90s declined 10% relative to 2018.” Because the Permian is the largest source of shale production and the most important source of growth, whatever happens there will determinate the trajectory for U.S. production figures on the whole.

Raymond James said that a slight uptick in productivity on an IP-30 basis but a decline on an IP-90 basis suggests that well interference is taking a toll. In other words, shale well performance is suffering as time goes on because wells have been spaced too close together. “Put another way, the average decline curve is becoming steeper than we thought because the wells are starting to cannibalize each other,” the analysts wrote.

Parent vs Child Wells

Problems with “parent-child” well interference have become more of a concern over the past year or so, which refers to the first well drilled within a given block (the parent well), and subsequent wells drilled (the child wells). As Raymond James notes, not only do they cannibalize each other, but the longer the parent is online, the more the block sees a drop in pressure.

But here’s the thing – a lot of companies have drilled parent wells on various tracts, incentivized to do so because their leases can expire if they don’t demonstrate activity. They held off on the child wells, focusing on drilling parents. Then, at a later point, they go back and drill child wells to squeeze more oil from their acreage. The problem is that so much of the output growth over the last few years came from parent wells. Going forward, the growth will need to increasingly come from the less productive child wells.

But as Raymond James notes, the longer they wait, the less productive the child wells become because the area loses more and more pressure over time.

In specific terms, the average child well is 30 percent less productive than the parent. But a child well, drilled six months after the parent may only see a 10 percent degradation in productivity, while a two-year delay might result in more substantial 40 percent reduction in productivity.

On the other hand, the “cube development” approach, which entails intense development all at the same time, also has problems. Cube development consists of multiple wells, often rising to more than a dozen, are drilled pretty much simultaneously to avoid well interference and pressure decline. Also, in theory, costs are lower because it takes less time, while shared infrastructure reduces costs as well.

But well interference still occurs, and a growing number of companies have reported disappointing results, suggesting that there are limits to density. In a high-profile admission just a few weeks ago, Concho Resources said its 23-well “Dominator” project proved disappointing. The company said it would space out its projects more. Raymond James says there is some middle ground on well-density that companies still need to figure out, but because the industry has boasted about ever-increasing well-density, the pullback is translating into stagnating productivity.

Ultimately, the investment bank says that because of weaker-than-expected productivity, U.S. oil production may only grow by around 350,000 bpd in 2020, versus the market consensus of around 1.5 million barrels per day. In a scenario in which productivity actually falls to zero, production would remain flat for the next few years.

Because “the single most important driver of the oil market over the next decade will be trends in U.S. well productivities,” Raymond James analysts wrote, this is “VERY bullish for oil prices next year.”

“Given that the oil market seems to be pricing in virtually unlimited U.S. oil supply growth at $50/bbl over the next five years, the implications…are very, very important to upside oil price surprises over the coming years.”

By Nick Cunningham of Oilprice.com

Link to original OilPrice.com article (Reprinted by Permission)

You might also like: