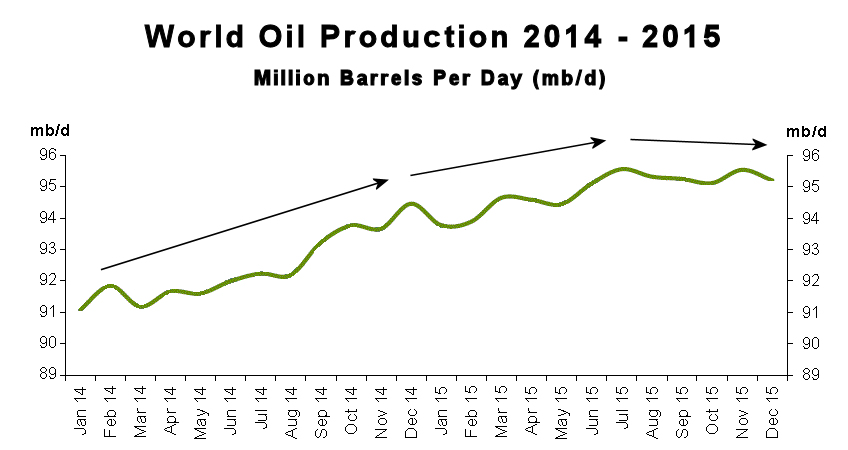

Commodities Overtake Stocks and Bonds with Best Rally Since 2010!

Traders who follow the price of gold and silver, should keep an eye out on the U.S. dollar index. Once the dollar starts to show signs of increased volatility (top) similar to 2000 – 2001 money will find its way into other currencies and precious metals as the new trade and safe haven.

Commodities Overtake Stocks and Bonds with Best Rally Since 2010! Read More »