While common sense tells us “printing our way to prosperity” seems like an unlikely longer-term outcome, in the short run it can help push stock prices higher. From Bloomberg:

The global currency wars are heating up again as central banks embark on a new round of easing to combat a slowdown in growth. The European Central Bank cut its key rate last week in a decision some investors say was intended in part to curb the euro after it soared to the strongest since 2011. The same day, Czech policy makers said they were intervening in the currency market for the first time in 11 years to weaken the koruna. New Zealand said it may delay rate increases to temper its dollar, and Australia warned the Aussie is “uncomfortably high.” With the outlook for the global economy being downgraded by the International Monetary Fund and inflation slowing to levels that may hinder investment, countries and central banks are revisiting policies that tend to boost competitiveness through weaker currencies.

The global currency wars are heating up again as central banks embark on a new round of easing to combat a slowdown in growth. The European Central Bank cut its key rate last week in a decision some investors say was intended in part to curb the euro after it soared to the strongest since 2011. The same day, Czech policy makers said they were intervening in the currency market for the first time in 11 years to weaken the koruna. New Zealand said it may delay rate increases to temper its dollar, and Australia warned the Aussie is “uncomfortably high.” With the outlook for the global economy being downgraded by the International Monetary Fund and inflation slowing to levels that may hinder investment, countries and central banks are revisiting policies that tend to boost competitiveness through weaker currencies.

Race To The Bottom

If every country tries to devalue their currency at the same time, it can become the battle of the printing presses. According to Wikipedia:

Races to the bottom can be described in game theory by the prisoner’s dilemma, originally framed by Merrill Flood and Melvin Dresher working at RAND in 1950. This is an exercise in which the optimal outcome for the entire group of participants results from cooperation of the participants, but it is put in danger by the fact that the optimal outcome for each individual is to not cooperate while the others do cooperate.

The term currency war is often tossed around in the financial press; what exactly does it mean and how can it harm growth in the long run? From Wikipedia:

Currency war, also known as competitive devaluation, is a condition in international affairs where countries compete against each other to achieve a relatively low exchange rate for their own currency. As the price to buy a particular currency falls so too does the real price of exports from the country. Imports become more expensive. So domestic industry, and thus employment, receives a boost in demand from both domestic and foreign markets. However, the price increase for imports can harm citizens’ purchasing power. The policy can also trigger retaliatory action by other countries which in turn can lead to a general decline in international trade, harming all countries.

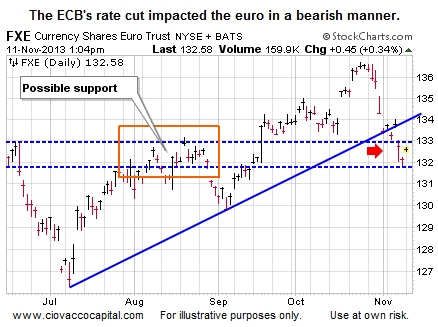

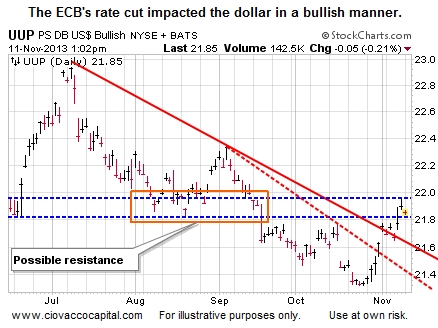

European Rate Cut Bolsters Taper Later Case

If the ECB prints money in the hope of driving down the value of the euro, the Fed must consider doing the same or face a strengthening dollar, which can negatively impact U.S. exports. At a minimum, the ECB’s actions last week make it more difficult for the Fed to begin tapering. Tapering means “print less money”. If the Fed decides to push out their first taper announcement, it means more money will be injected into the global financial system via quantitative easing (QE). As explained in this QE video, the new cash in the financial system can act as a source of demand for stocks.

Investment Implications

Last week’s better than expected labor report and Wall Street’s expectation for a renewed clash in the currency wars support the case for a risk-on investment allocation. While we are still holding positions in the United States (SPY), Europe (FEZ), and globally (VT), we would feel better if cyclical leadership returned. The weekly charts continue to paint a thin-leadership picture. Despite our short-term concerns about leadership, as we outlined in this weekend’s stock market outlook video, the longer-term case for equities remains positive. The S&P 500’s 50-day moving average recently turned back up (see A below), which indicates an improving intermediate-term trend. Stock bulls would prefer to see the recent breakout near point B hold this week; stock bears are hoping the S&P 500 will drop back below the pink trendline.

See Also:

- The Difference Between FIAT and Real (Music and Gold)

- The MI-5 Guide to Foreign Exchange Risk

- Is the Dollar Really King?

- Surviving a Hyperinflation

Chris Ciovacco is the Chief Investment Officer for Ciovacco Capital Management, LLC (CCM). This article contains the current opinions of the author but not necessarily those of CCM. The opinions are subject to change without notice. This article is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Copyright © 2013 Ciovacco Capital Management, LLC. and has been reprinted by permission and originally appeared here.